How Sustainable is my Insurance Policy?

A recent study by the ZHAW School of Management and Law has revealed the sustainability preferences of private policyholders, but the majority cannot tell whether their policy is sustainable or not.

Everyday items are usually easier to evaluate. For example, food often has sustainability declarations on its packaging and electrical goods come with an energy consumption label. But what about insurance policies? Over 40 percent of respondents could not say whether their insurance companies are committed to sustainability. This is confirmed in a survey of almost 1,500 Swiss residents conducted by the ZHAW School of Management and Law in collaboration with EY and BearingPoint. Trust in insurance companies regarding sustainability is not conspicuous, and only a handful of policyholders are willing to pay more for sustainable insurance.

Possible reasons for a sobering status quo

“Sustainability is very abstract in insurance,” says Corina Grünenfelder, Head of Sustainable Finance at audit and consulting company EY. “Customers ask themselves, ‘What do I need to look out for? The fact that my invoice is sent electronically instead of on paper cannot be everything. Do I understand how my premiums are invested? Will I receive a more ecologically friendly replacement in the event of a claim? Can my insurer help prepare me for environmental and social changes?’ The variety of topics can be confusing and client advisors are usually unprepared for such a discussion,” explains Grünenfelder. “At the moment, being committed to sustainability has little resonance with customers,” says Claudio Stadelmann, partner at management and technology consultancy BearingPoint. “Specialized teams are driving the issue, but this has not yet permeated the entire organization.” In addition, as part of the financial market, there is only limited trust in insurance companies concerning social commitment. “No wonder so few people are willing to pay more for a sustainable policy right now,” observes Stadelmann.

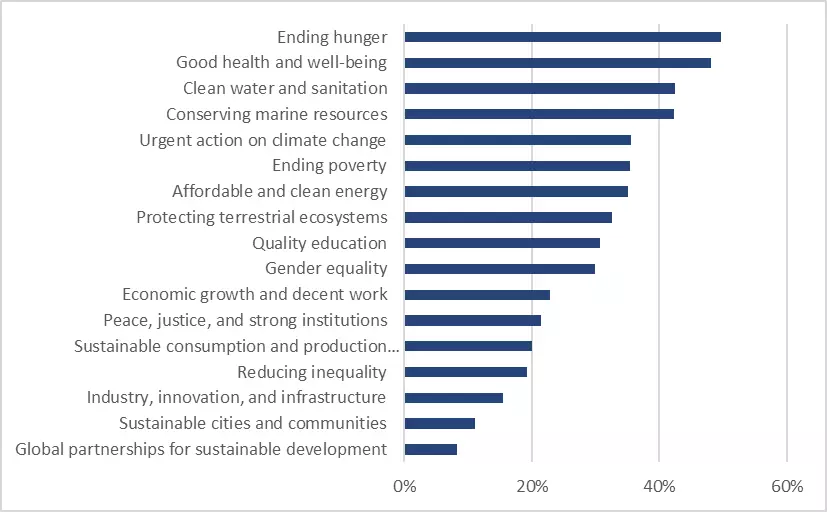

Do not neglect social issues

When sustainability is mentioned, it is often in the context of the climate. However, the survey shows that social issues are rated more highly than environmental issues when prioritizing the UN’s 17 Sustainable Development Goals (SDGs).

“There is significant potential for insurers to score points on sustainability. That’s because sustainability is actually very close to the idea of insurance in terms of social balance and across generations,” says study lead Lukas Stricker from the ZHAW Institute for Risk & Insurance. Also, as risk management professionals, insurers should find ways to share this expertise with their customers. Products related to protecting oneself from natural hazards or dealing with them better were weighted higher in the survey than activities aimed at reducing one’s own ecological footprint. Another critical factor is the claim itself – which is when the hitherto virtual insurance product materializes. How will a damaged item be treated? Will it be repaired rather than replaced in the spirit of the circular economy? And if so, will it be replaced with an ecologically superior product, even if it costs more? Here, insurers can send clear messages through their product design and contractual partners, who are also perceived by customers because there is a clear association between them.

Sustainability should be more central

Those responsible for conducting the study agree that the issue of sustainability must be increasingly moved from committees and boardrooms to the customer. “Frequently, sustainability only concerns the directors and senior managers of Swiss insurance companies. Otherwise, it is restricted to specialist teams and the investment department,” says Lukas Stricker. “Client advisors should be trained accordingly and raise the profile of sustainability in insurance.” Another suggestion from the study coordinators is establishing an independent insurance sustainability label to help those buying policies make better-informed choices.

Contact

Lukas Stricker, Institute for Risk & Insurance, ZHAW School of Management and Law, Phone +41 (0)58 934 74 62, email lukas.stricker@zhaw.ch

Valerie Hosp, Communications, ZHAW School of Management and Law, Phone +41 (0)58 934 40 68, email valerie.hosp@zhaw.ch